VISITORS

News & Events

Products are always designed towards convenience for customers

VBSP has studied and developed appropriate services for its customers who are vulnerable population living in rural and disadvantaged areas and have limited access to commercial bank products and services. In addition to implementing Government-designated credit programs to various clients, VBSP has designed savings products specifically for the poor through Savings and Credit Groups. In 2019, VBSP's savings outstanding balance reached VND 22,340 billion (USD 971 thousand). In which, the deposit balance from Savings and Credit Group members is VND 10,098 billion, accounting for 45% of total savings outstanding balance, with 6 million members participating. The balance of savings deposits mobilized at commune transaction points reached VND 3,345 billion, accounting for 15% of the total saving outstanding balance.

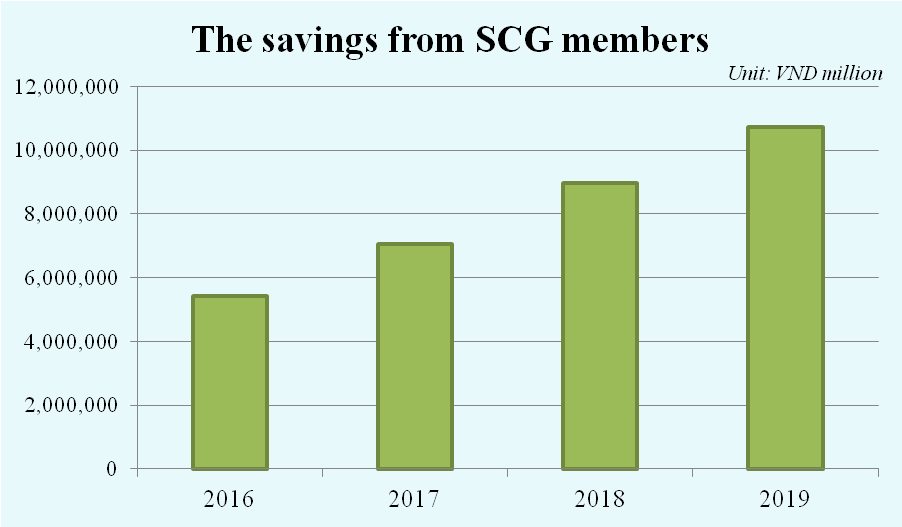

The mirco-savings deposit service for the poor through savings and credit groups on one hand helps the borrowers practice saving habits, increases income and repayment ability, on the other hand, create favorable conditions for the poor and policy beneficiaries to access banking services. The figure shows the increase in saving amount from SCG members very quickly, which indicates the positive efficiency of VBSP target on savings products.

In addition, since 2016, Vietnam Bank for Social Policies has implemented a savings mobilization service for residents at commune transaction points. Instead of going to a bank office, which is far away from place of living, people in rural areas can deposit their savings into the Social Policy Bank at the Commune Transaction Point. This product brings convenience to customers living away from the urban centers, contributing to mobilizing resources from the public and providing banking products and services to rural areas..

The latest product has been launched in 2019 is the flexible saving deposit. The product is designed for all eligible customers to deposits many times during the saving terms with the flexible amount each. With the favorable condition, the poor and low income segment even are not active borrowers at VBSP can access to VBSP services and practice saving with a small amount on demand.

One of the regular products is demand deposit. This type of saving services is used mainly for making payment transactions via banks by means of payment such as checks, payment orders, e-transfer.. The benefits from demand deposit are simple and quick signing up procedure and easy deposit and withdrawal. Also, the transfer fee is low which is suitable and attracted to the active borrowers and community, especially the vulnerable group.

- The Board of Directors of the Vietnam Bank for Social Policies Holds the Regular Meeting for the First Quarter of 2026

- Bringing digital banking services closer to the people of Thanh Hoa province

- Amplifying the impact of preferential credit in An Giang Province

- A reliable source of preferential credit supporting improvements in people’s quality of life

- Supporting disadvantaged individuals in rebuilding their lives

- Expanded preferential credit access creates more opportunities for workers to take up employment abroad

- A solid support for people seeking a second chance

- Study Visit of the Bankers Institute of Rural Development (BIRD) to Vietnam

- RDB Visits and Works with VBSP

- Policy credit empowers women to rise and stabilize their livelihoods

- VBSP altogether prevent against Corona virus disease (COVID-19)

- VBSP provides various credit schemes for the poor and other last mile population

- VBSP broadens banking service network and channels

- Newsletter Vol 16

- Financial inclusion: Empower Vietnamese women

- Poor households are supported to access VBSP's inclusive finance

- Effective credit policy for ethnic minority

- VBSP conducted the exposure visit to India on learning digital finance transformation

- Resources mobilized to improve livelihoods of the poor

- Disadvantaged laborers given help to work abroad

- The Board of Directors of the Vietnam Bank for Social Policies Holds the Regular Meeting for the First Quarter of 2026

- VBSP Promotes Digital Transformation by Organizing 03 - Information Security Training Sessions for Staff

- Bringing digital banking services closer to the people of Thanh Hoa province

- Amplifying the impact of preferential credit in An Giang Province

- A reliable source of preferential credit supporting improvements in people’s quality of life

- Supporting disadvantaged individuals in rebuilding their lives

- Expanded preferential credit access creates more opportunities for workers to take up employment abroad

- A solid support for people seeking a second chance

- Study Visit of the Bankers Institute of Rural Development (BIRD) to Vietnam

- RDB Visits and Works with VBSP

LENDING INTEREST RATE

|

||||||||||||||||||||

DEPOSIT INTEREST RATE

|

||||||||||