VISITORS

Press Release

Methods of social policy credit lending and management

(VBSP News) VBSP's social credit schemes are carried out according to credit schemes under Decisions and Decrees promulgated by the Prime Minister and the Government for each individual or a group of specific target customers. Here are two methods VBSP applied for social policy credit lending and management.

VBSP's specific social policy credit lending and management methods

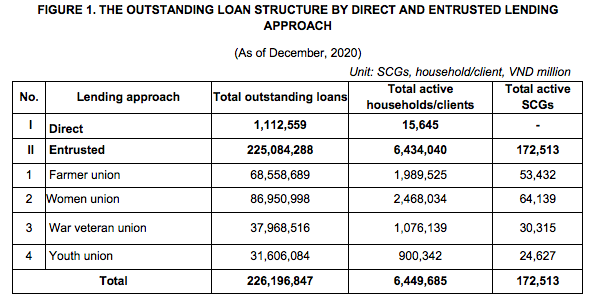

1. Entrusting some steps in the lending process for local mass organizations, SCGs and integrating credit with agricultural, forestry & aquaculture extension models

The entrusted tasks taken over by four mass organizations

They conduct communication on social policy credit schemes, support SCG management and group member enrollment, follow up SCG’s operation, check loan use, collaborate with VBSP to organize commune transaction, training SCGs leader and members, integrate credit with agricultural, forestry and aquacultural extension, technological & scientific transfer and other community activities in order to ensure effective business and production, contributed to loan use for proper purpose.

For the collateral-free loan schemes, the borrowers shall join SCGs that include 3-60 members/group in the same village location.

Both SCGs and entrusted mass organizations at commune level will conduct some steps in the lending process, for instance: communication on social policy credit schemes, customer selection, instruct customers arrange loan applications, appraisal of feasible borrowing projects, estimate credit request and check loan utilization. SCG leaders are authorized to collect monthly loan interest, micro-savings of group members, concile and support to make applications for loan restructuring and risk treatment due to objective reasons as well as loan repayment reminders.

The collaboration/mentor model with SCGs and local mass organizations in social policy credit conduction has contributed to cut down on transaction costs with a large number of micro-loan customers while the number of staff is limited as regulated, bringing about effective and efficient loan disbursement, repayment and quality.

2. Model of VBSP’s commune transaction point

Nearly 80% VBSP’s operation is conducted in over 10,000 commune transaction points nationwide. Commune transaction is performed once per month on a fixed day by field staff teams (3-5 pax/team) from district branches in the venue of communal People’s Committee with some key activities: loan disbursement, loan collection and deposit in order to facilitate customers living in remote, mountainous and rural areas to access financial services conveniently, fast, save time and travelling cost for them. The transaction cost of VBSP can increase up, however, the community/society’s cost reduces considerably.

The decentralization of management, information exchange and processing aims to overcome limitations due to the large number of customers and micro-loan accounts with the partnership between VBSP - Mass organizations - SCGs - Customers. Currently, VBSP is also upgrading the core-banking system and investing the mobile banking system to gradually increase loan transactions, collect non-cash debt and reduce transaction costs in the future.

- VBSP promotes green inclusive finance towards sustainable development

- VBSP offers preferential loans to students, master’s students, and doctoral candidates in science, technology, engineering, and mathematics (STEM) fields

- Annual Report 2023

- The VBSP’s Board of Directors (BOD) held its regular meeting for the fourth quarter of 2024

- Annual Report 2022

- VBSP implements tasks for the year 2025

- Credit policies under Decision 22 for ex-prisoners to rebuild lives in Ha Nam

- Households in disadvantaged areas can borrow up to VND 100 million for business and production.

- VBSP's Trade Union worked with the Korean Finance Union delegation

- Promotion of digital financial services to enable financial inclusion for the disadvantaged population in Vietnam

- Poverty mitigation efforts prove highly effective

- Social policy credit for each different objective and beneficiary, serving the national target programs

- VBSP’s operational strategy and sustainable development goals

- Newsletter Vol 09.2021

- VBSP supports Covid-19 affected employers

- The effectiveness of the policy capital in Huong Son district in recent years

- Some 145 billion VND disbursed to pay salaries for production resumption

- VBSP actively supports production & business households, SMEs in disadvantaged areas

- Businesses supported with loans to pay salaries and restore production

- Escape from poverty thanks to preferential credit capital

- Building Livelihoods through Preferential Credit in Lao Cai: From Chickens and Homestays to the Dream of Escaping Poverty

- VBSP PROGRESS REPORT Q1/2026

- The Board of Directors of the Vietnam Bank for Social Policies Holds the Regular Meeting for the First Quarter of 2026

- VBSP Promotes Digital Transformation by Organizing 03 - Information Security Training Sessions for Staff

- Bringing digital banking services closer to the people of Thanh Hoa province

- Amplifying the impact of preferential credit in An Giang Province

- A reliable source of preferential credit supporting improvements in people’s quality of life

- Supporting disadvantaged individuals in rebuilding their lives

- Expanded preferential credit access creates more opportunities for workers to take up employment abroad

- A solid support for people seeking a second chance

LENDING INTEREST RATE

|

||||||||||||||||||||

DEPOSIT INTEREST RATE

|

||||||||||